Introduction

In the world of long-term financial planning, structured settlements have played an important role for decades. They are designed to provide stability, predictability, and financial security over time—especially for individuals who have received compensation from personal injury cases, insurance claims, or legal settlements.

However, life does not always follow a predictable schedule. Economic conditions change, personal priorities evolve, and unexpected opportunities or challenges arise. As a result, many settlement recipients begin to explore a critical question:

Is it possible—and financially responsible—to access cash now from a structured settlement?

This article offers a clear, CEO-friendly, and professional overview of what it means to get cash now for a structured settlement. It is written to inform, not persuade, and focuses on helping readers understand the strategic, financial, and long-term implications of this decision.

Whether you are a settlement recipient, a financial decision-maker, or someone researching long-term income strategies, this guide provides balanced insights to support informed choices.

Understanding Structured Settlements

What Is a Structured Settlement?

A structured settlement is a financial arrangement in which compensation from a legal or insurance claim is paid out over time rather than in a single lump sum. These payments are typically scheduled monthly, annually, or at specific intervals and may last for years or even decades.

Structured settlements are commonly used in:

- Personal injury cases

- Medical malpractice claims

- Workers’ compensation settlements

- Wrongful death cases

The core purpose is financial protection—ensuring consistent income while reducing the risk of mismanagement or rapid depletion of funds.

Why Structured Settlements Were Created

Structured settlements were developed to address common financial challenges faced by recipients of large lump-sum payments. Without structure, recipients may:

- Overspend early

- Make high-risk investments

- Struggle with long-term budgeting

By providing scheduled payments, structured settlements aim to:

- Encourage long-term financial stability

- Protect vulnerable recipients

- Reduce emotional decision-making

From a design standpoint, structured settlements prioritize security over flexibility.

Why People Consider Getting Cash Now

Despite their advantages, structured settlements are not always aligned with real-world needs. Over time, many recipients reconsider their financial structure.

Life Changes and Financial Reality

Common reasons individuals explore cash access include:

- Medical expenses not covered by insurance

- Education or tuition costs

- Home purchases or renovations

- Business or investment opportunities

- Debt consolidation

- Major life transitions

These needs may require immediate liquidity—something structured payments are not designed to provide.

Opportunity Cost and Timing

From a strategic perspective, receiving money later has a cost. Inflation, missed investment opportunities, or rising expenses can reduce the real value of future payments.

Some recipients view accessing cash now as a way to:

- Take advantage of time-sensitive opportunities

- Reallocate capital more strategically

- Regain financial control

This is not necessarily about dissatisfaction—but about adaptation.

How Accessing Cash from a Structured Settlement Works

Selling Structured Settlement Payments

In many jurisdictions, recipients are legally allowed to sell some or all of their future structured settlement payments in exchange for a lump sum of cash today.

This process is commonly referred to as:

- Structured settlement factoring

- Payment transfer

- Settlement sale

It is regulated and typically requires court approval to ensure the transaction is fair and in the best interest of the recipient.

Partial vs. Full Transfers

Recipients do not always need to sell their entire settlement.

Options often include:

- Selling a portion of future payments

- Selling payments for a fixed period

- Retaining long-term income while gaining short-term liquidity

This flexibility allows individuals to balance immediate needs with future security.

The Legal and Regulatory Framework

Court Approval and Consumer Protection

Structured settlement transfers are governed by law in many countries, particularly in the United States. Courts review proposed transactions to ensure:

- Transparency

- Fair valuation

- No coercion or exploitation

This oversight exists to protect recipients from unfavorable agreements.

Disclosure and Due Diligence

Before approval, recipients typically receive:

- A full breakdown of payment value

- Discount rates applied

- Net amount to be received

- Comparison to original settlement value

This process reinforces informed decision-making rather than impulse choices.

Financial Considerations: A Strategic View

Understanding the Discount Rate

When future payments are converted into present cash, a discount rate is applied. This rate reflects:

- Time value of money

- Risk factors

- Market conditions

- Administrative and legal costs

The result is that the lump sum received is less than the total future value of the payments.

From a CEO perspective, this is not a loss—it is a trade-off between certainty and liquidity.

Weighing Immediate Value vs. Long-Term Stability

The decision should not be framed as “good” or “bad,” but as strategically appropriate or not, depending on context.

Key questions to consider:

- What problem does immediate cash solve?

- Is this problem temporary or structural?

- What alternatives exist?

- How will future income be replaced or managed?

Strong decisions are made with clarity, not urgency.

When Getting Cash Now Makes Strategic Sense

Scenario 1: High-Impact Opportunities

Accessing capital may enable:

- Business investments

- Career advancement

- Education with strong ROI potential

If the long-term benefit outweighs the reduced future payments, the decision may be justified.

Scenario 2: Financial Stress Reduction

Eliminating high-interest debt or addressing urgent expenses can:

- Improve mental well-being

- Restore financial balance

- Reduce compounding financial risk

In some cases, stability now is more valuable than income later.

Scenario 3: Changing Risk Profile

As individuals mature financially, their risk tolerance and priorities evolve. What made sense at one life stage may not align with current realities.

When Caution Is Required

Emotional or Short-Term Decision-Making

Decisions driven by pressure, fear, or impulse often lead to regret. Structured settlements exist to protect against this exact scenario.

A pause for reflection and consultation is essential.

Lack of Financial Planning

Selling payments without a clear plan for using the funds can create long-term vulnerability. Cash without strategy often disappears faster than expected.

The Role of Professional Advice

Financial Advisors and Legal Counsel

Before proceeding, many recipients consult:

- Financial planners

- Attorneys

- Tax professionals

These experts help evaluate:

- Long-term impact

- Opportunity cost

- Risk management

- Tax considerations

Independent advice strengthens decision quality.

Tax Implications

In many cases, structured settlement payments are tax-free, and lump sums received from approved transfers may also be non-taxable. However, rules vary by jurisdiction and circumstance.

Professional confirmation is always recommended.

A CEO-Friendly Decision Framework

Executives and leaders approach financial decisions with structure. The same mindset applies here.

Step 1: Define the Objective

What is the cash needed for—and why now?

Step 2: Analyze Trade-Offs

What is being exchanged for liquidity?

Step 3: Assess Risk

What happens if the funds are misused or underperform?

Step 4: Plan Deployment

How will the cash be allocated, managed, or invested?

Step 5: Preserve Optionality

Is it possible to retain some future payments?

Ethical and Long-Term Responsibility

Financial freedom comes with responsibility. Accessing settlement funds is not simply a transaction—it is a strategic life decision.

Responsible decision-making includes:

- Transparency

- Education

- Long-term thinking

- Protection of future needs

When approached thoughtfully, flexibility does not have to compromise security.

The Bigger Picture: Financial Empowerment

Structured settlements were designed to protect recipients—but empowerment also means choice.

Having the ability to adapt financial structures to real-world needs is a sign of maturity in financial systems. The goal is not to eliminate structure, but to align it with evolving life goals.

Conclusion

Getting cash now for a structured settlement is neither inherently right nor wrong. It is a strategic option that, when evaluated carefully, can serve as a valuable financial tool.

For decision-makers, the focus should remain on:

- Clarity over urgency

- Strategy over emotion

- Long-term resilience over short-term relief

By understanding the mechanics, implications, and responsibilities involved, individuals can make confident, informed decisions that align with both present needs and future security.

Financial leadership—whether in business or personal life—is about making choices that stand the test of time.

Summary:

When you agreed to the terms of your structured settlement you accepted a series of financial payments that made sense for you at that time but is that still the case?

Keywords:

structured settlement, structured settlements, sell structured settlement, buy structured settlement

Article Body:

If you�ve agreed to accept a structured settlement, it�s likely that you felt a sense of relief that your financial uncertainties were being resolved, and that you�d have the funds necessary to pay your bills, support your family and go on with your life. When you agreed to the terms of the settlement, hopefully with the help of a financial advisor, you accepted a series of financial payments that made sense for you at that time.

Perhaps you�d suffered personal injury in an auto or other accident, you were awarded damages in a product liability case, or you were the victim of medical malpractice or were even the plaintiff in a wrongful death suit. You agreed to a periodic (usually monthly) payment, maybe in the form of a lifetime income stream, that seemed to be the answer to paying your ongoing living expenses and perhaps your medical costs. You made the best decisions you could at the time, with the information you had � based upon how life was then, and what you expected for the future.

But life seldom works out as we expect. Maybe you�re on the road to recovery from the accident or other event for which you received the settlement, and want to move and buy a house, get married, go to school, or buy a business. Maybe medical bills or high interest debt is an undue burden on you that you need to resolve now. Or, if your family has grown, and your children no longer need for you to provide for their education or other expenses, you may want to spend more of the money you have coming to you now, instead of later.

What can you do to match your finances � specifically your structured settlement � with the life you now have or want to have? You should always consult an attorney or a financial advisor, but here�s a basic overview of your rights and options in assigning your structured settlement:

Settlements are funded by single premium annuities, issued by insurance companies. Instead of paying you a lump sum amount, the party found responsible for injury or damages to you has paid a one-time lump sum to an insurance company, which has, in turn, invested it. The insurance company has projected the interest rate or securities dividends they will receive on the lump sum, and based upon the length of time and number of payments you chose or were offered for the structured settlement, they calculated the periodic payment amount you�re now receiving.

So who owns what? The insurance company owns the annuity, and you, as the beneficiary, are entitled to an income stream, or the series of periodic payments. Because you don�t own the underlying asset, the annuity, you therefore can�t sell the annuity contract to another party to receive your money. However, under federal and state law you can, with court approval, sell all or a portion of the payments you are entitled to receive in the future. In doing so, you can receive a lump sum cash payout now.

What are your options? As an annuitant, or the beneficiary of the structured settlement annuity, you are, in most instances, able to assign to a third party the payments you are entitled to receive in the future. Some Structured Settlement Agreements state that payments cannot be assigned, and your legal counsel will advise you of options and alternatives if yours is written with such a clause. Fortunately, state laws and recent case law have rendered contracts written with such provisions unenforceable, although other regulations may apply.

How can you determine today�s lump sum value of your structured settlement payments? This depends, in part, upon the amount of each payment and when it is due. The payment amount and schedule will be outlined in your Structured Settlement Agreement. It is also affected by the financial strength of the issuer of your annuity, because the better the financial position of the issuer, the more likely it is that the purchaser of your cash stream will be paid. The current financial climate, as well as interest rates will also affect your cash-out amount. Your financing company will explain these calculations and assumptions to you.

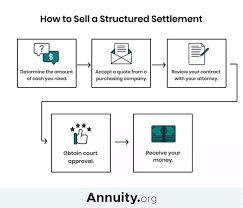

What steps do you need to take?

- First, you really need to take a hard look at whether receiving your funds now will truly be best for you and your family. This is a big financial step, not to be taken lightly. That said, your circumstances may have changed sufficiently so that a lump sum or partial payment in the form of a lump sum makes sense, and is better for your family�s current and future lifestyle and financial stability.

- Next, contact a reliable financing company that purchases structured settlement income streams. They can guide you through the process and help you consider alternatives, such as the sale of a portion of your structured settlement income stream, if this best meets your needs.

- The financing company will assist you by hiring an attorney experienced in structured settlement assignments. The attorney will explain to the court your desire to change your settlement, and any changes in your life that have caused you to make this decision. Because the attorney will be petitioning for judicial approval, he will need to understand your current finances, obligations and desires.

- Having all your documentation and agreements, and furnishing them promptly to your advisors and potential funding sources is key to receiving a cash payout in the shortest possible time. Because court approval is required, the time from the initiation of the request to the final approval is typically 45-90 days. So, just as with other large financial decisions, such as obtaining a mortgage or refinancing, it�s in your best interest to begin the process with a little time to spare, before you feel a time crunch. You deserve an equitable deal, as quickly as is possible, not just the deal you can make in the very least amount of time.

- What can you expect now? Once you have chosen a finance company and attorney, the courts will put you on the docket and hear your petition for receiving your funds in a lump sum. They�ll want details of the future payments due you, the proposed amount of the lump sum distribution, and any costs you will incur as a result of restructuring your settlement. Their basis for granting you an approval is satisfying themselves that the assignment of your payments to another party and receipt of current cash will be in your best interest and in the best interests of any dependents you may have.

- Once you�ve agreed upon a lump sum amount with your finance company, and obtained court approval, you�ll receive a wire transfer or a cashier�s check for your lump sum amount. You�ll now have the cash you need � right when you need it most.

Tinggalkan Balasan