In today’s fast-paced digital economy, managing finances efficiently has become more important than ever. One of the most strategic financial moves for individuals and businesses alike is obtaining an offshore bank account. Traditionally, setting up an offshore account involved complex paperwork, in-person visits, and extensive bureaucracy. However, with the rise of the internet and digital banking solutions, getting an offshore bank account online has never been easier. In this article, we will walk you through everything you need to know—from understanding the benefits, choosing the right jurisdiction, to completing the application process online safely and legally.

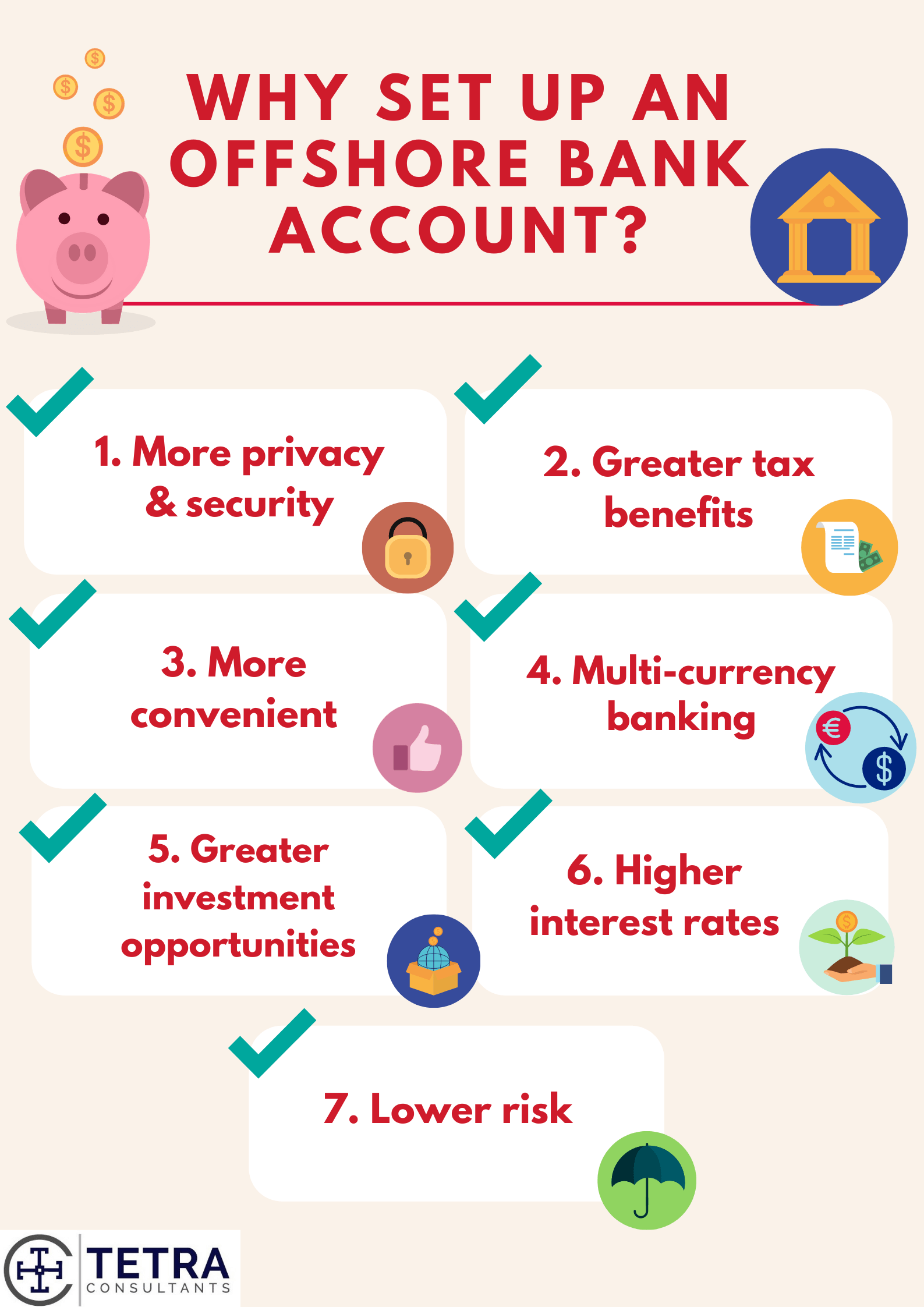

Why Consider an Offshore Bank Account?

Before diving into the mechanics of opening an offshore bank account online, it’s essential to understand why so many individuals and businesses consider this option:

1. Diversification of Assets

Keeping all your funds in a single domestic bank account can be risky. Offshore banking allows you to diversify your assets across different financial jurisdictions, which can protect your wealth from economic instability or political uncertainty in your home country.

2. Access to International Financial Services

Offshore banks often offer services that may not be readily available in your country, such as multi-currency accounts, investment opportunities, and specialized financial instruments. These services can provide flexibility for both personal and business financial management.

3. Tax Optimization (Legal)

While offshore accounts are sometimes associated with tax evasion, the legal use of offshore accounts focuses on tax efficiency and proper planning. Many jurisdictions offer favorable tax rates or no tax on certain types of income, but it’s crucial to remain compliant with your home country’s regulations.

4. Privacy and Security

Offshore banks are often situated in jurisdictions with strong privacy laws. While they do comply with international anti-money laundering regulations, they also provide a higher level of confidentiality than standard domestic accounts.

5. Ease of International Transactions

If you frequently travel, run an international business, or deal with clients across borders, an offshore account can make international transactions faster and cheaper. Many offshore banks provide lower fees and better exchange rates for cross-border transfers.

Choosing the Right Jurisdiction

Not all offshore banking jurisdictions are created equal. The choice of jurisdiction can affect everything from account maintenance fees to regulatory oversight and account security. Here are some popular options:

1. Switzerland

Switzerland has long been synonymous with financial privacy and stability. It offers strong banking laws, multi-currency accounts, and access to sophisticated financial services.

2. Singapore

Singapore is highly regarded for its economic stability and strong regulatory framework. Its banks provide high-quality online banking services and robust asset protection features.

3. Cayman Islands

The Cayman Islands is a tax-neutral jurisdiction, making it popular for investment purposes. Offshore accounts here are often used by corporations and high-net-worth individuals for international business transactions.

4. Belize

Belize offers simplified online account opening procedures, making it attractive for individuals looking for a straightforward process. The jurisdiction also provides a high degree of privacy.

5. Panama

Panama combines privacy with favorable banking laws and is often chosen for international business accounts. Online account opening has become more streamlined in recent years.

When choosing a jurisdiction, consider factors such as banking fees, ease of online access, legal protections, and international reputation.

Requirements for Opening an Offshore Bank Account Online

Opening an offshore account via the internet is simpler than the traditional process but still requires careful preparation. Typical requirements include:

- Valid Identification Documents – Passport, national ID, and sometimes driver’s license.

- Proof of Address – Utility bill, bank statement, or government-issued document dated within the last three months.

- Bank Reference Letter – A letter from your existing bank confirming your account history and financial standing.

- Source of Funds Declaration – Proof of income or funds, such as salary slips, tax returns, or business invoices.

- Application Form – Completed online form provided by the bank.

Many banks also conduct due diligence checks to ensure compliance with international anti-money laundering laws.

Step-by-Step Process to Open an Offshore Account Online

Step 1: Research and Choose a Bank

Not all offshore banks accept online applications from non-residents. Look for banks that specialize in digital account openings and have a strong reputation. Read reviews, check regulatory compliance, and compare services.

Step 2: Prepare Your Documentation

Ensure all your documents are up to date, clearly scanned, and meet the bank’s requirements. Digital submission is standard, so clarity is key.

Step 3: Complete the Online Application

Most banks offer a secure portal where you can upload documents and fill in your personal and financial information. Accuracy is essential to avoid delays.

Step 4: Verification Process

Banks often perform video calls to verify your identity. Some may request notarized documents, but many modern banks accept digital notarization.

Step 5: Fund Your Account

After approval, you’ll need to make an initial deposit. Minimum deposits vary depending on the bank and account type. Multi-currency accounts may allow you to deposit in USD, EUR, GBP, or other currencies.

Step 6: Access Your Online Banking

Once funded, you can access your account through secure online banking platforms. Offshore banks usually provide services such as wire transfers, debit cards, online payments, and investment accounts.

Summary:

There is no need to use the many middleman websites you will find via a search engine.

Keywords:

Offshore bank account, offshore banking

Article Body:

There is no need to use the many middleman websites you will find via a search engine. Most of these are bogus, even the slick-looking ones. More and more banks are offering offshore bank accounts direct. Just get a list of banks in the country you’re interested in, and go to their web sites.

Opening an offshore bank account is like opening one in your high street; meet their criteria, and you’re in. The only difference is you’re not there in person.

The first thing is to find out whether they will accept citizens or residents of your country. For example, Swiss banks tend not to want US customers; they don’t want the hassle from the IRS.

You will need to prove your identity, and the legal existence of your company, if you wish to open an account for it.

If applying by mail, DO NOT PART WITH ORIGINAL DOCUMENTS. Get copies notarised by a notary public. Originals can be used for fraud or identity theft. Or they can get lost.

A Notary Public is a public officer commissioned by the State to perform notarial acts. A Notary is an impartial witness. The notary is empowered to issue an apostille.

Apostille – Is a method of certifying a document for use in another country pursuant to the 1961 Hague Convention. With this certification by apostille, a document is entitled to recognition in the country of intended use, and no certification or legalization by the embassy or consulate of the foreign country where the document is to be used is required.

In practice this means you provide evidence to this man that you are who you say you are, and/or that your company is what you say it is. You take an oath on the Bible. That’s right, it’s not a joke.

Due diligence: Banks need to show they have checked who their customers are, and how they came by their money.

Passport – If you apply by post a notarised copy is needed;

Information about yourself – name, date of birth, address, phone number etc.

Your economic background – documents showing how you earn your money (work contract, bank statement, tax return, company documents);

Origin of your deposits – documents showing how you earned them. If you sell a house, proof of the sale, a copy of the estate agent’s listing, and so on;

Information about your deposits – how much you plan to deposit, and what you plan to do with the money once you’ve banked it.

If opening a company account, you send an apostilled copy of the certificate of incorporation to the bank providing your account, along with evidence of your identity, an application form, and any other documents they ask for.

If you want to get an offshore bank account, consider visiting the bank in person. If you can, travel to the country in question, and open a bank account there. You probably live near one tax haven at least. This especially applies if you are planning to deposit large sums; find out who you’re dealing with!

NOTES:

- Don’t pay a middleman to open a bank account for you. See above.

- Do not use services which offer bank accounts in Eastern European countries.

You are likely to be cheated, possibly by the bank itself. Avoid Latvia!

- Avoid web sites where:

The business address is a P.O. Box, or a ‘Suite’;

The site is on a free web host;

The site is badly translated into English;

You have the sense you are dealing with Africans or Eastern Europeans;

The site has not been updated recently e.g. the Copyright reads 2001;

They’ve only been running for a few years;

They offer a range of dubious products – second passports, citizenships, anonymous debit cards;

You cannot pay via credit card – it’s much harder to get refunds on banker’s drafts, Western Union and e-Gold etc;

They require you sign a confidentiality agreement, or you have the sense you are entering quasi-legal or illegal territory.

Bogus offshore banking sites can threaten to report you to your tax authority if you question their methods. It’s an old con trick; get the mark involved in something illegal, then he can’t go to the authorities.

Offshore bank accounts and company formations are just like their onshore equivalents; there’s no big mystery about them. If you want a company formation, contact a local registration agent, who speaks English, in the country of registration. Then use another local agent to check what the first one’s done.

Open your bank account yourself.

One last thing: don’t think that because your bank account and company are offshore you can do business in your home country, and/or with fellow residents, and avoid taxes there.

You’ll find plenty of websites that’ll purport to help you, right up until the time you get a small brown envelope from your country’s tax inspectors, inviting you in for a little chat.

Tinggalkan Balasan